Worthune’s Smart Beta Investing Strategy Guide for Wealthy Investors:

If you are a wealthy investor, your advisors may have brought up the concept of Smart Beta or Smart Beta Investing. For investors with a significant footprint in the stock market, it is essential to understand the idea of smart beta and the smart beta products in the marketplace.

What is Smart Beta and Smart Beta Investing Strategy? Smart Beta explained in simple terms:

Smart Beta Investing (also known as advanced beta or fundamental indexing or factor investing) is an investing strategy that tries to combine the transparency and low cost of traditional indexing and a rules-based portfolio construction process that looks beyond the conventional indexing which relies on market capitalization as the sole driver.

Smart Beta Investing Strategy tries to blend the tenets of CAPM (Capital Asset Pricing Model) with the constructs of Value Investing and relies on an open and transparent set of rules on how to select and rebalance the stocks in the portfolio.

The specific strategy of a smart beta can range from simple investing themes to complex factor-based portfolio models. Technically, any portfolio construction that does not rely on the price/weight of a stock is a smart beta product. But in the industry, the most common styles of smart beta are fundamental weighting, volatility weighting, quality weighting, momentum-driven, dividend weighting, and equal weighting.

Some credit Research Affiliates, investment management firm, for the concept and yet others credit Towers Watson, a professional services firm, for the term. And some other market pundits credit Harry Markowitz with the idea. Either way, while the name may be new, many firms, particularly institutional investors, have been investing in this format for several decades.

What is Traditional Indexing (or Market-Cap-based Indexing) and what flaws are necessitating Smart Beta Strategies?

Traditional Indexing or market-cap-based indexing is a revolution in the world of investing allowing investors to stop their reliance on active money managers and their often expensive and underperforming strategies and instead on a portfolio strategy that is a representation of a broad market index.

For example, if there are only four stocks in an investing universe, and each one is equal regarding its weight in an index, then the index fund will own 25% of each of these stocks. (Most indices are market capitalization weighted, except the Dow Jones Industrial Average, which is a price-weighted index.)

On average, more than 80% of the active managers underperform their benchmark index. Often, this is a combination of misplaced bets and higher expenses. And even the 20% or so that outperform the index may not do it on a constant basis. (Of course, there are always exceptions such as Peter Lynch, Warren Buffet or Bill Miller who are folk heroes in the sphere of active management.) Hence, the concept of indexing has become popular, notably as John Bogle and Vanguard championed the cause through the creation of low-cost index funds and many decades later, the ETFs (Exchange Traded Funds.) According to MorningStar, at the end of 2017, nearly 45% of the total AUM (Asset under management) are in passive strategies.

The advantages of investing in indices are severalfold – instant diversification, low cost, capture the broad representation of the stock universe, and transparency.

The disadvantages or flaws in this approach are as follows: A) If you invest with the market in an index, you will never overperform the index. B) The index investing makes sense when two assumptions – that markets are efficient and investors are rational – hold. C) The massive influx of monies into index investing causes issues around price discovery and liquidity profile of underlying index components.

Furthermore, many investors feel like they can do better than the indices and hence alternative portfolio construction processes, while holding the costs as low as possible, led to the creation of portfolios/funds/ETFs based on Smart Beta.

What are some examples of Smart Beta Portfolio Strategies?

Smart beta products rely on the concept of a “Factor.” A factor is any underlying attribute, characteristic, or a parameter that is known to drive the stock performance. Firms leverage one or more of these factors to formulate a theme and construct a portfolio with a set of rules for allocation and rebalancing – each of which becomes a smart beta or a factor product. For example, contemporary investment analysts deem the style of investing that Graham and Dodd are famous for – the value investing – a factor model or a smart beta strategy.

While there are hundreds of factors to consider, many academic and industry research studies show that most factors do not yield long-term, stable, and enduring outperformance. So, while companies continue to experiment with the value and validity of diverse elements, here are a few that have shown to produce long-term results and hence many firms adapt these to build factor models or smart beta products.

Value: Value investing means finding inexpensive stocks that are trading below their intrinsic worth and holding them for the long-term until the market catches up. Similarly, one can use value as a factor and construct a portfolio that tilts a portion of the portfolio toward undervalued stocks.

Momentum: It’s tough to argue against momentum akin to a snowball becomes an avalanche. A streak of recent strong performance tends to be a positive indicator for future stock performance. (Unless of course, the momentum stops.)

Fundamentals: Companies that have shown constant growth and a strong balance sheet are good candidates for superior returns. Hence, fundamentals such as revenue growth, operational earnings, free cash flow, and other measures are influential factors.

Liquidity: Anything that is scarce tends to feel its more valuable. And same is the case with stocks with lower liquidity which are typically to perform stronger – when all other things being equal.

Volatility: Stocks that are less volatile, while may provide a lower absolute return, tend to deliver better risk-adjusted returns.

Multi-Factor: While a smart beta strategy may employ only one factor, in reality, many portfolios tend to depend on a cluster of factors, thus making multi-factor smart beta portfolios a preferred option.

Will Smart Beta Strategies Outperform the Market or the Traditional Index-based Funds/Portfolios/ETFs?

There are absolutely no guarantees that a specific factor (and consequently such factor particular portfolios) will outperform the market. Different elements tend to outperform during certain time periods. If your portfolio is swimming against the tide with a factor strategy that is out of sync with the times, then it is very likely that your smart beta strategy will not look as bright.

One must remember that a well-diversified portfolio that spans different asset classes, geographies, sectors, and time horizons is still the best strategy. Factor investing or smart beta strategies are just the icings on the cake to seek better outcomes.

For example, an investor assumes value investing is the optimal portfolio construction method, but that style of investing and the stocks that belong to that strategy may underperform for several years. In that case, the portfolio will yield lower returns.

What is the risk of investing in smart beta portfolios or factor-based products?

Similar to any other investment products, smart beta products or factor-based portfolios are NOT a fool-proof method against losses. To summarize the risks are:

Loss of Principal: One can lose all their money when there is a market downturn (unless your factor strategy involves shorting the market) and systematic macro risk will affect the portfolios.

Purchasing Power: Choosing factors that are very low in volatility may also mean lower absolute returns and this may cause diminished purchasing power.

Extended Periods of Underperformance: Even if the stock markets have blockbuster years, a portfolio that bets on wrong factors may witness prolonged underperformance.

Liquidity: If a particular factor leads to investments in physical assets or illiquid assets, lack of liquidity and absence of a dynamic market may lead to challenges in price discovery, and the ability to sell promptly.

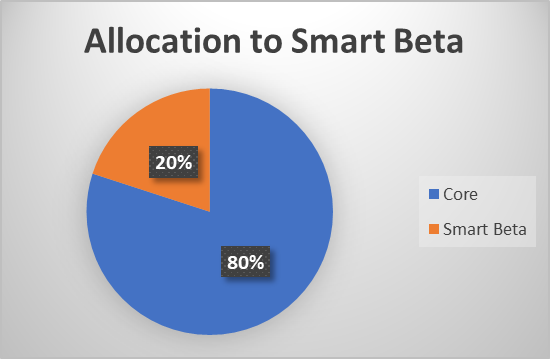

How much of my net worth should be in Smart Beta Products?

It is a tough question as some purists, a diversified core portfolio with some tilts may mean that the entire portfolio is a factor-based or smart beta portfolio. However, while it depends on the personal financial situation, risk tolerance, time horizon, investment sophistication, and overall net worth of each or family, a general rule of thumb is to invest 80% in core assets that are a broad representation of the markets across asset classes, styles, markets, and sectors, and then use 20% toward specific tilts to bolster the performance.

General Rule of Thumb: Percentage of the portfolio in Smart Beta Products

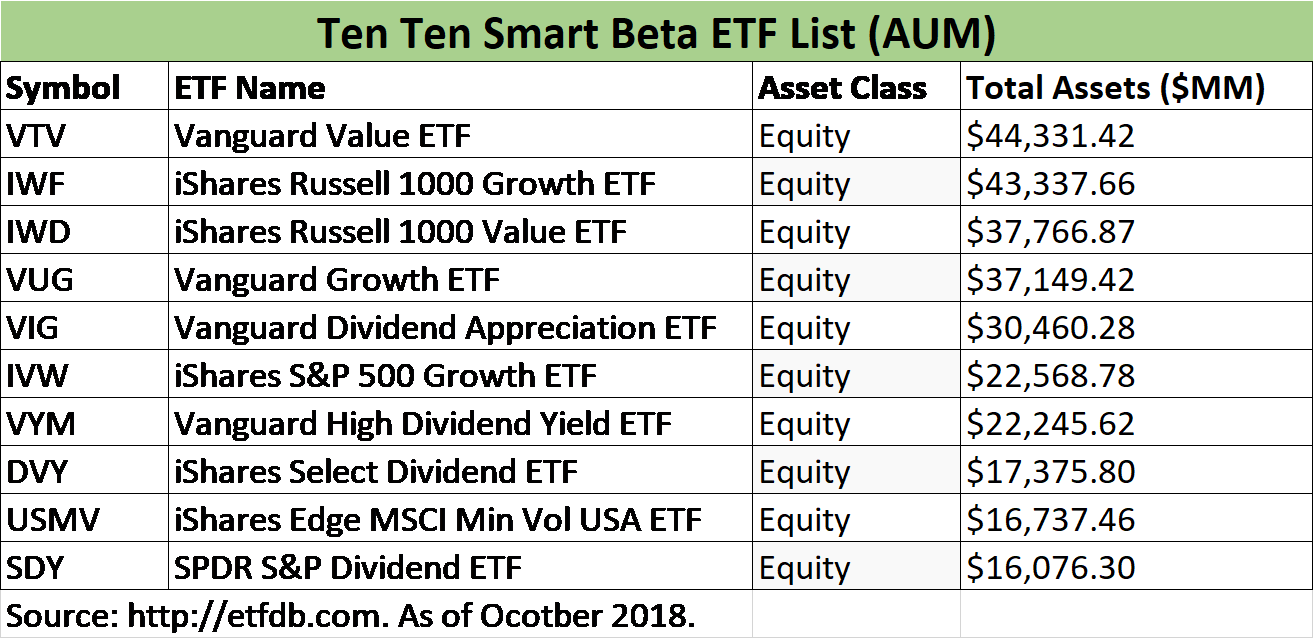

What are top Smart Beta ETFs?

The following are the top Smart Beta ETFs, based on the AUM (Asset Under Management), which are employing smart beta strategies or factors in constructing their portfolio. As new products come into the market and inflows and outflows affect the existing smart Beta ETFs, please ensure you are looking at the latest data before making an investment decision.

What are some of the top firms offering smart beta ETFs or Smart Beta Funds?

Some of the top asset management firms offer a smart beta or factor products – some as ETFs, or Institutional Portfolios, or Mutual Funds. Each vehicle has a distinct profile, and a smart investor needs to conduct due diligence into each product before making an informed decision.

Vanguard Smart Beta or Factor Products:

Vanguard is one of the largest asset managers in the world and a pioneer of low-cost index funds. Vanguard offers several smart beta portfolios (or factor products). At the time of writing this article, Vanguard has a list of six ETFs and two mutual funds that employ smart beta investment strategies.

VFVA: U.S. Value Factor ETF

Stocks with low prices relative to fundamentals.

VFMO: U.S. Momentum Factor ETF

Stocks that demonstrate strong short-term performance.

VFQY: U.S. Quality Factor ETF

Stocks of companies with stronger operational earnings and balance sheet quality.

VFLQ: U.S. Liquidity Factor ETF

Stocks that are less frequently traded than more liquid securities.

VFMF: U.S. Multifactor ETF

Multifactor stocks offering diversification benefits garnered through merging equity factor tilts.

VFMV: U.S. Minimum Volatility ETF

Stocks with lower volatility with the potential for improved risk-adjusted returns.

VFMFX: U.S. Multifactor Fund Admiral

Multifactor stocks offering diversification benefits garnered through merging equity factor tilts.

VMNVX: Global Minimum Volatility Fund

Stocks with lower volatility with the potential for improving risk-adjusted returns than the global equity market.

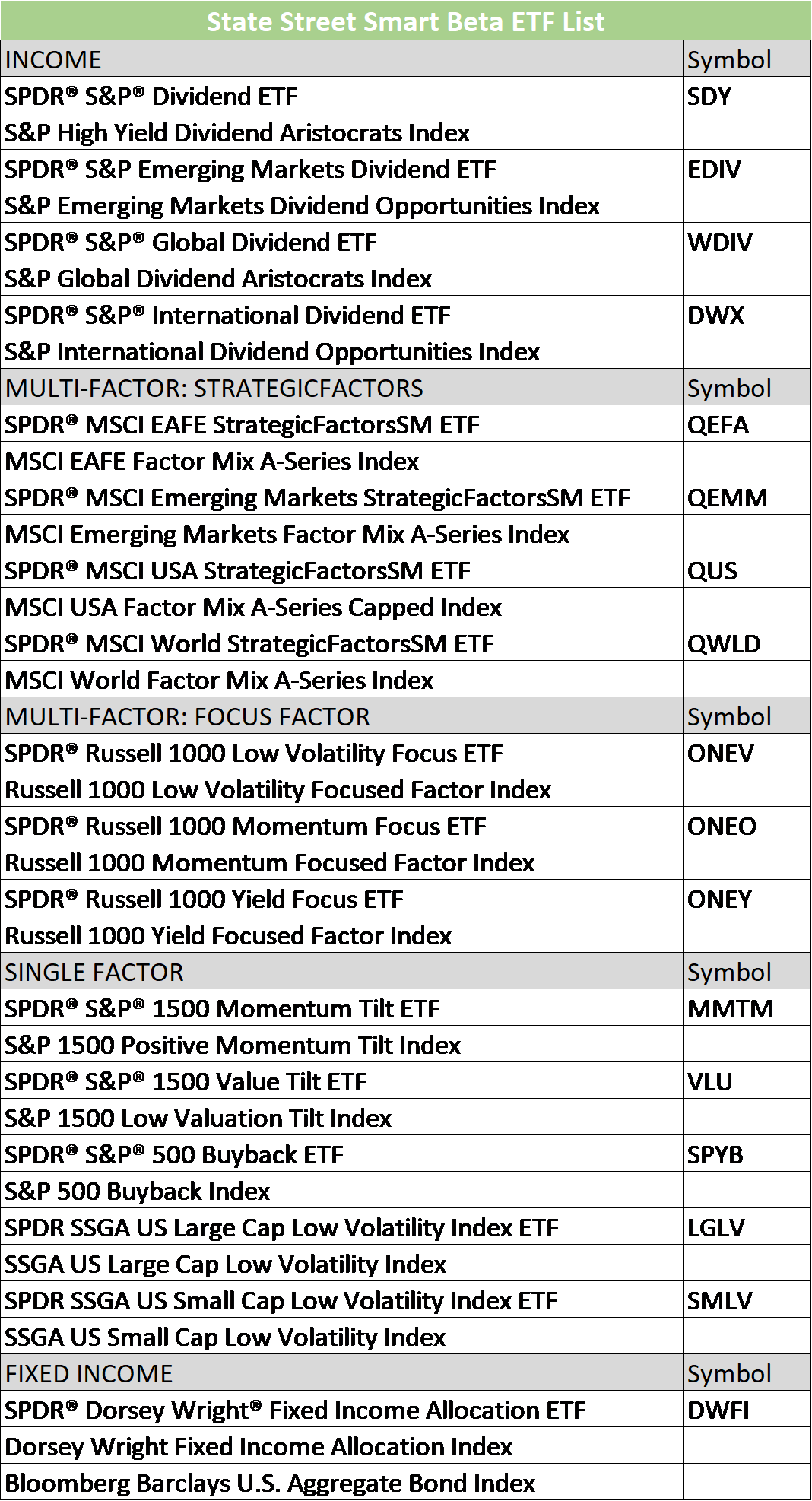

State Street Smart Beta ETFs:

State Street is a pioneer in the ETF space and now has several smart beta offerings as a part of its vast array of products. Below is a broader list of ETFs that State Street is classifying as smart beta or factor products.

Research Affiliates Smart Beta Products:

Research Affiliates is an investment research advisory firm that some credit with pioneering or at least bringing to the mainstream the concept of factor investing or smart beta.

RAFI Multi-Factor:

RAFI Multi-Factor is a smart beta equity strategy that offers diversified factor exposures through allocations to value, low volatility, quality, momentum, and size.

RAFI Fundamental Index:

RAFI Fundamental Index is built on the principles of contrarian investing and disciplined rebalancing.

RAFI ESG:

RAFI ESG strategies combine the pioneering Fundamental Index approach with thoughtfully designed environmental, social, and governance investment themes.

RAFI Low Volatility:

FTSE RAFI Low Volatility seeks to efficiently reduce equity risk while maintaining attractive valuations and broadly diversified market exposures.

RAFI Equity Income:

FTSE RAFI Equity Income seeks to produce sustainable dividend income through a diversified smart beta strategy that selects high quality, high dividend paying stocks.

RAFI Commodities: Dow Jones RAFI Commodities seeks to deliver inflation protection, portfolio diversification, and excess returns in a low-cost smart beta strategy.

RAFI Bonds:

RAFI bond indices use a transparent rules-based methodology to weight bonds using economic measures of company or country size and are thus tilted toward higher credit-quality firms or countries with lower risk of downgrade or default.

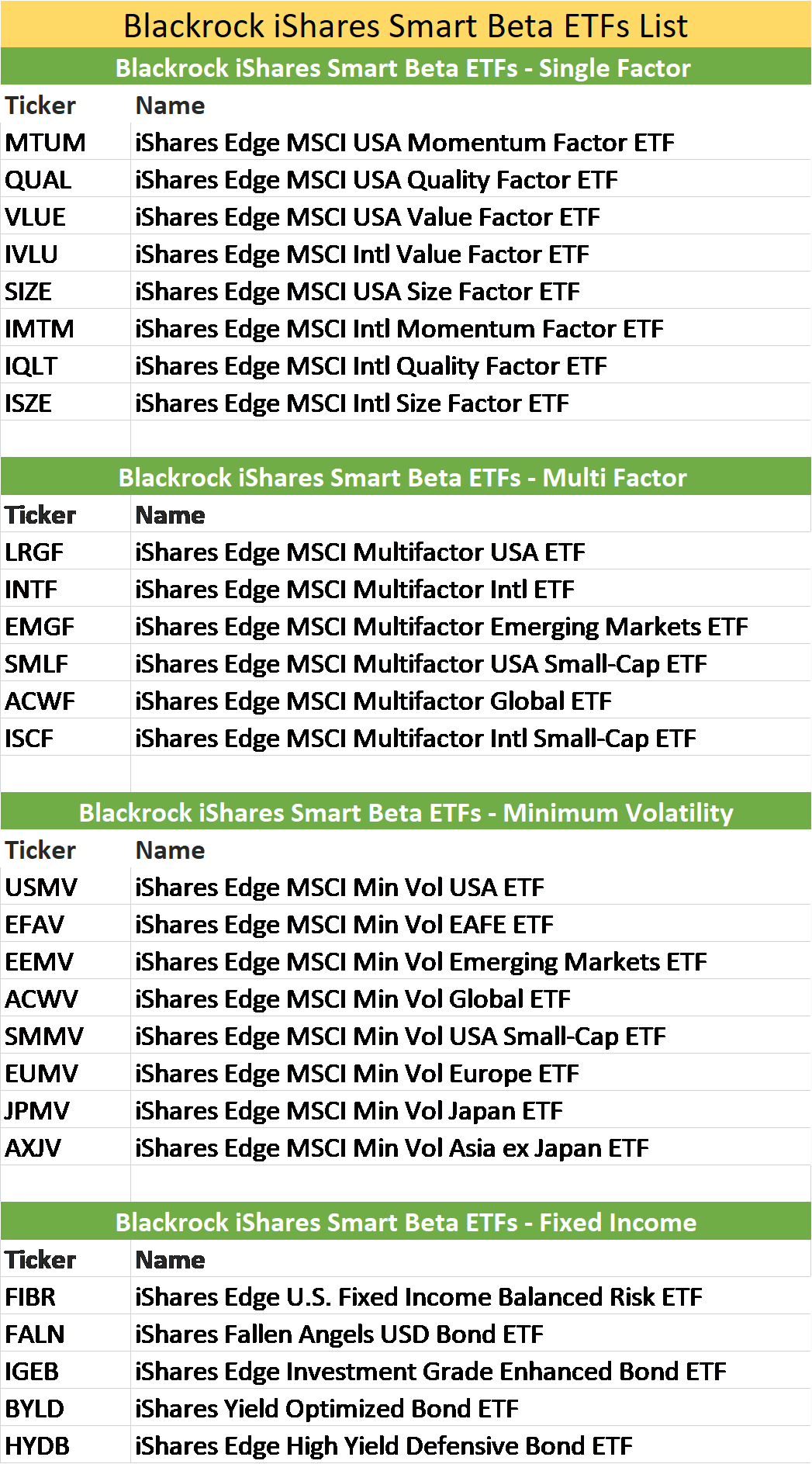

Blackrock iShares Smart Beta ETF List:

Blackrock is the largest money manager in the world and is the owner of the iShares ETFs family. Blackrock has recently shut down several smart Beta ETFs, but it still offers a range of factor products across single factor, multiple factors, minimum volatility, and fixed income factors.

Further Reading and Resources about Smart Beta Investing Strategy:

Disclaimers:

The Smart Beta Investing article is for informational purposes only. Investing in smart beta products involves risk of loss of principal. Please consult your financial, tax, and legal advisors for how smart beta investing strategy may fit into your overall wealth optimization. While we strive to provide quality information, we cannot guarantee the accuracy or efficacy of the data in the article. Please conduct your due diligence before making any investment decisions. All products and company names are respective trademarks of the companies, and a mention does not constitute an endorsement on either side.

Leave A Comment